The reopening income tax assessments under Section 147 of the Income Tax Act has always been a contentious issue. The recent Supreme Court judgment in M/s. Mangalam Publications, Kottayam vs. Commissioner of Income Tax, Kottayam sheds light on critical aspects of this provision, especially concerning reassessments based on omitted or incomplete material facts.

This blog delves into the key takeaways from the case, offering actionable insights for businesses and individuals.

The Case at a Glance

Parties Involved:

- Appellant: M/s. Mangalam Publications (a newspaper publishing business).

- Respondent: Commissioner of Income Tax, Kottayam.

Key Issue: Can assessments be reopened if the taxpayer failed to disclose certain facts, or if the Assessing Officer (AO) forms a new opinion based on existing facts?

Judgment: The Supreme Court ruled in favor of the taxpayer, restoring the Tribunal’s order that deemed the reassessments invalid.

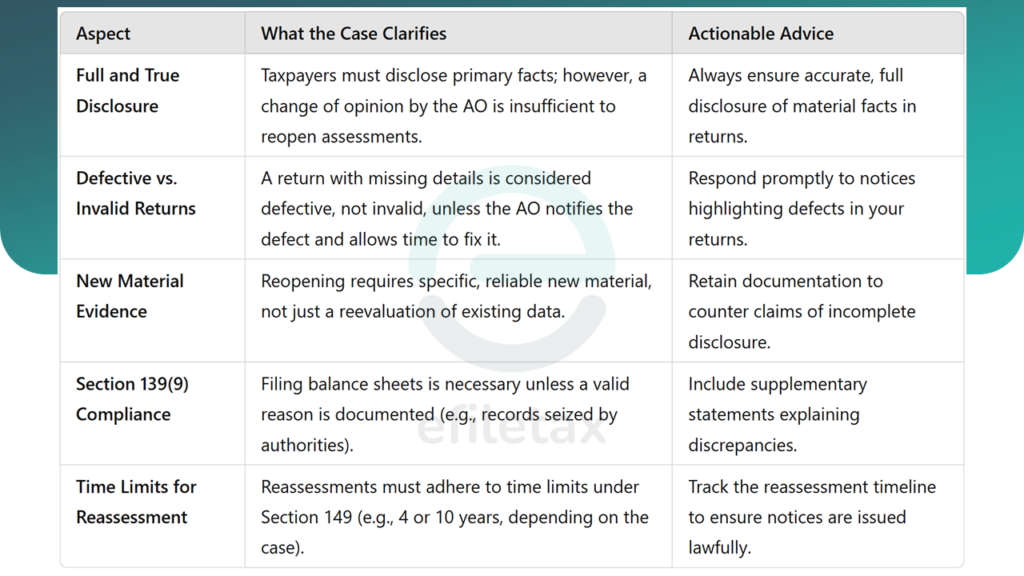

Key Learnings for Taxpayers

Why This Matters

The decision reinforces taxpayer rights, curbing the misuse of reassessment provisions for fishing expeditions. However, it also emphasizes the importance of complete disclosures during the initial assessment to avoid unnecessary litigation.

The Mangalam Publications case serves as a pivotal reminder of the safeguards built into the Income Tax Act for reopening assessments. Taxpayers and businesses must proactively comply with disclosure norms while defending their rights against unwarranted reassessments.