Who Should Opt for GST Rule 14A and When Businesses Should Avoid It

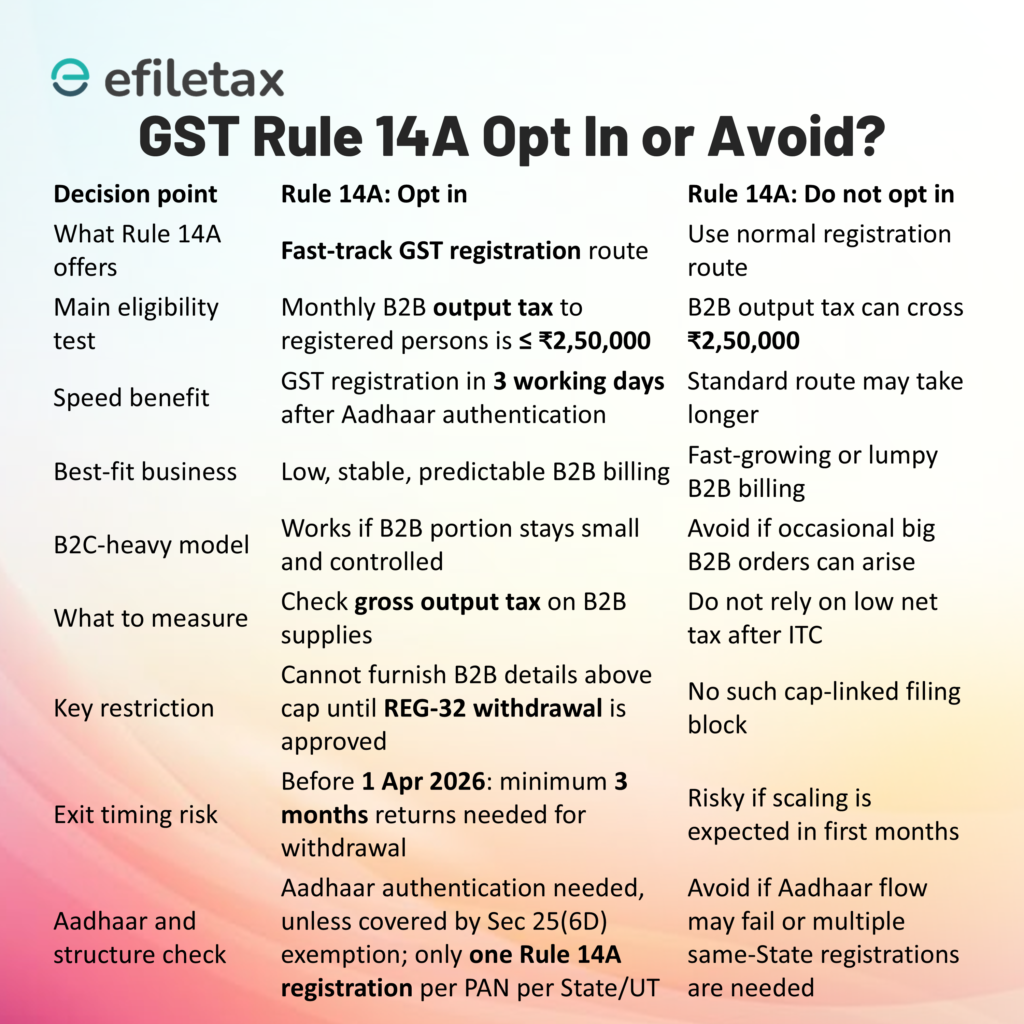

India’s GST framework introduced Rule 14A under the CGST Rules, 2017, effective 1 November 2025, to provide a fast-track GST registration option for eligible businesses.

Under this option, applicants can receive their GSTIN within 3 working days, significantly faster than the normal GST registration process, which may take 7 days or even up to 30 days depending on verification requirements.

However, the faster approval comes with an important operational restriction — a monthly cap of ₹2.5 lakh on B2B output tax liability. Because of this limit, choosing Rule 14A should be a carefully considered business decision rather than simply a quicker administrative process.

What Is GST Rule 14A?

Rule 14A introduces an optional GST registration pathway for taxpayers who self-assess that their monthly output tax liability on B2B supplies will not exceed ₹2,50,000.

The cap includes the combined amount of:

- CGST

- SGST / UTGST

- IGST

- Compensation Cess (if applicable)

It is important to understand that the limit applies to gross output tax on B2B transactions, not the total turnover or the net tax payable after Input Tax Credit (ITC).

This means that even businesses with higher turnover may qualify if their B2B output tax remains within the prescribed limit.

How the Rule 14A Fast-Track Registration Works

The process under Rule 14A typically follows these steps:

1. GST Registration Application

While filing Form GST REG-01, the applicant selects the Rule 14A option and self-declares that their monthly B2B output tax liability will remain within ₹2.5 lakh.

2. Aadhaar Authentication

Applicants opting for this fast-track registration route must complete Aadhaar authentication, usually through OTP or biometric verification.

3. GSTIN Issued Within 3 Days

Once the verification is completed successfully, the GST portal generally issues the GSTIN within three working days.

4. Operating Within the B2B Output Tax Cap

After registration under Rule 14A, the taxpayer cannot report B2B output tax exceeding ₹2.5 lakh per month on the GST portal.

5. Withdrawal from Rule 14A

If the business grows and exceeds the cap, the taxpayer must apply for withdrawal using Form GST REG-32.

After approval through Form GST REG-33, the taxpayer can start reporting higher B2B output tax from the first day of the following month.

Important Compliance Risk Under Rule 14A

Many businesses assume that the ₹2.5 lakh limit applies to turnover or net tax payable, but this is incorrect.

The limit applies to gross output tax on B2B supplies before adjusting ITC.

This means:

- Even if Input Tax Credit offsets most of the tax, the cap may still be breached.

- Businesses with large B2B invoices may cross the limit quickly.

- The GST portal may restrict reporting of B2B invoices once the threshold is reached.

Therefore, businesses opting for Rule 14A must carefully monitor their B2B tax liability every month.

Businesses That Benefit From Rule 14A

Rule 14A may be suitable for businesses with predictable and limited B2B tax exposure.

Examples include:

Small Service Providers and Professionals

- Consultants

- Freelancers

- Marketing agencies

- Job workers

Startups That Need GST Registration Quickly

Early-stage startups often require quick GSTIN approval for vendor onboarding or compliance.

Predominantly B2C Businesses

Retailers or service providers with mostly consumer sales but occasional B2B invoices may safely operate within the tax cap.

Who Should Avoid Rule 14A?

While the fast-track registration option appears attractive, it may not be suitable for all businesses.

Fast-Growing B2B Businesses

Businesses with fluctuating revenue or large project invoices may exceed the tax cap unexpectedly.

Businesses With High Output Tax

Companies issuing large B2B invoices may cross the output tax threshold even if ITC offsets the liability.

Businesses Planning Expansion

Only one Rule 14A registration per PAN per State is allowed, which could restrict operational flexibility.

Businesses Expecting Rapid Growth

Businesses anticipating strong growth may find the withdrawal process inconvenient if the limit is breached frequently.

Quick Decision Guide for Businesses

| Situation | Rule 14A Suitable? | Reason |

|---|---|---|

| Freelancer or consultant with limited B2B clients | ✔ Suitable | Output tax likely within cap |

| Startup needing quick GSTIN | ✔ Suitable | Faster registration |

| Retailer mainly selling to consumers | ✔ Suitable | Minimal B2B tax exposure |

| Manufacturing company selling to distributors | ✖ Not suitable | High B2B tax exposure |

| Businesses expecting rapid growth | ✖ Risky | Output tax may exceed cap |

| Companies issuing large B2B invoices | ✖ Not recommended | Cap may be breached quickly |

Compliance Responsibilities Under Rule 14A

Even though registration approval is faster, all standard GST compliance requirements continue to apply, including:

- Filing GSTR-1 (outward supplies return)

- Filing GSTR-3B (summary tax return)

- Timely payment of GST liabilities

- Updating bank account details within 30 days of registration

Non-compliance may result in interest, penalties, or cancellation proceedings.

Key Questions Businesses Should Ask Before Opting for Rule 14A

Before choosing this option, businesses should consider:

- Can the monthly B2B output tax liability be predicted reliably?

- Will large invoices or seasonal sales increase B2B tax exposure?

- Is the business primarily B2C or B2B?

- Is the business prepared to monitor the tax cap regularly?

A proper assessment ensures that businesses do not face operational restrictions later.

Conclusion

Rule 14A provides a faster route to GST registration, which can be extremely useful for startups and small businesses needing a GSTIN quickly.

However, the ₹2.5 lakh monthly B2B output tax cap means that this option may not be suitable for businesses with high-value B2B transactions or rapid growth plans.

Businesses should therefore carefully evaluate their customer mix, billing patterns, and growth projections before opting for Rule 14A.

How EFILETAX Can Help

At EFILETAX, our GST professionals assist businesses with:

- GST registration and advisory

- Evaluating whether Rule 14A is suitable for your business

- Monitoring B2B tax limits and compliance

- Filing GSTR-1 and GSTR-3B returns

- Handling Rule 14A withdrawal applications (REG-32)

If you need guidance on GST registration or compliance, our team can help you make the right decision for your business.