Introduction

Accounting is the language of business. Whether you’re a small business owner, a student, or someone managing personal finances, understanding accounting terms is essential. This blog breaks down accounting jargon into simple explanations, aligning with established accounting standards to ensure accuracy and relevance. Accounting Terms Simplified

Understanding Accounting Standards

Accounting standards are the rules and guidelines that govern how financial statements are prepared. They ensure uniformity, transparency, and accuracy in financial reporting. This guide simplifies accounting terms while maintaining compliance with standards like the Indian Accounting Standards (Ind AS) and International Financial Reporting Standards (IFRS).

Accounting Terms Explained

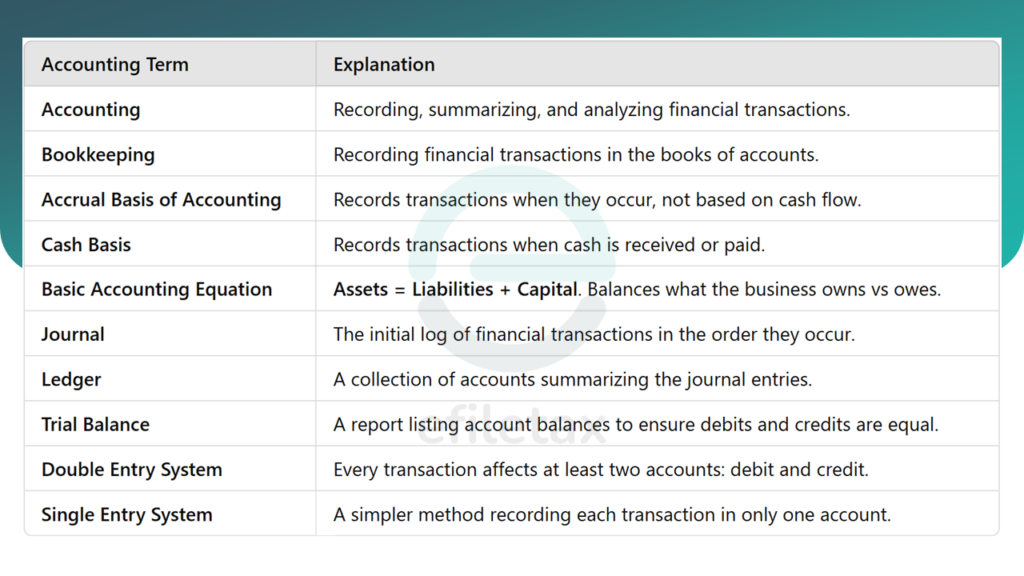

1. Accounting

Definition: The process of recording, summarizing, and analyzing financial transactions of a business.

Relevance to Standards: Accounting adheres to the accrual concept under Ind AS 1, ensuring all financial events are documented.

Example: Preparing a profit-and-loss statement to assess a company’s financial health.

2. Bookkeeping

Definition: The act of systematically recording all financial transactions.

Relevance to Standards: Complies with Ind AS 16 for maintaining accurate asset records.

Example: Logging every invoice and receipt in accounting software like Tally or Zoho Books.

3. Accrual Basis of Accounting

Definition: Transactions are recorded when they occur, regardless of when cash is received or paid.

Relevance to Standards: Mandated under Ind AS 18 (Revenue Recognition).

Example: A software company records revenue when a client signs a contract, even if payment is made later.

4. Cash Basis

Definition: Transactions are recorded only when cash is exchanged.

Relevance to Standards: Rarely used in corporate accounting but permitted for small businesses in certain jurisdictions.

Example: A bakery records sales only when customers pay at the counter.

5. Basic Accounting Equation

Definition: The foundation of accounting: Assets = Liabilities + Equity.

Relevance to Standards: Reflected in Ind AS 1 under the balance sheet structure.

Example: A business with ₹10 lakh in assets and ₹6 lakh in liabilities has ₹4 lakh in owner’s equity.

6. Journal

Definition: A chronological record of financial transactions.

Relevance to Standards: Forms the base for preparing financial statements as per Ind AS 1.

Example: Recording a ₹5,000 rent payment in the general journal.

7. Ledger

Definition: A collection of accounts summarizing journal entries.

Relevance to Standards: Used to create financial statements, adhering to Ind AS 10.

Example: The ledger groups rent payments under “Expenses” and sales revenue under “Income.”

8. Trial Balance

Definition: A report that checks if total debits match total credits.

Relevance to Standards: Ensures compliance with the Double Entry System under Ind AS 21.

Example: Before closing books, a company prepares a trial balance to ensure all accounts are balanced.

9. Double Entry System

Definition: Every transaction affects at least two accounts, maintaining balance between debits and credits.

Relevance to Standards: Fundamental to all accounting systems worldwide.

Example: Recording a ₹10,000 sale: Debit “Cash,” Credit “Revenue.”

10. Single Entry System

Definition: A simplified method where transactions are recorded only once.

Relevance to Standards: Not recommended for formal business accounting.

Example: Small shopkeepers use this system for personal bookkeeping.

FAQs on Accounting Terms

1. Why is accrual accounting preferred over cash basis?

Accrual accounting gives a complete financial picture by recording revenue and expenses as they occur, not just when cash is exchanged.

2. How does the trial balance ensure accuracy?

By ensuring total debits match total credits, a trial balance helps identify errors in the books.

3. Is single-entry bookkeeping enough for businesses?

Single-entry is simpler but lacks the depth and accuracy needed for decision-making in most businesses.

Key Takeaways

- Accrual vs Cash Accounting: Accrual is ideal for businesses; cash is simpler but less accurate.

- Double-Entry System: Mandatory for accurate financial records.

- Trial Balance: A crucial step before preparing financial statements.

Understanding these terms will empower you to make informed financial decisions and ensure compliance with accounting standards.