Capital gains exemption under Section 54F has long been debated—especially when the reinvested property has multiple floors. A recent Delhi High Court ruling has now cleared the air: different floors of a single residential house do not disqualify a taxpayer from claiming the full exemption.

Delhi HC clarifies that multiple floors of a single house don’t disqualify a taxpayer from claiming capital gains exemption under Section 54F. The judgment in favour of Lata Goel sets a precedent and simplifies the “one residential house” condition for capital gains reinvestments.

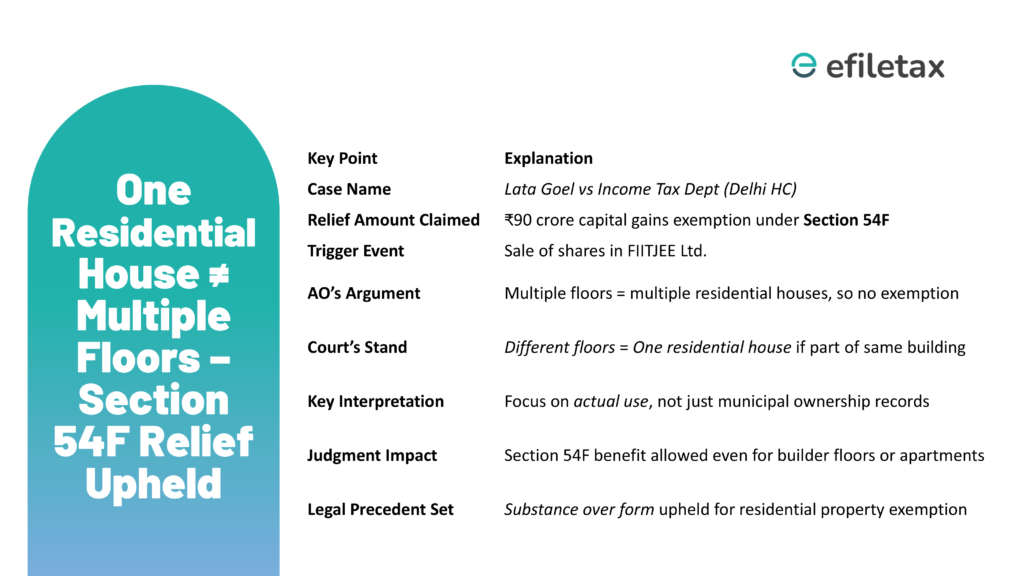

🔍 What Was the Case?

- Assessee: Lata Goel, wife of FIITJEE promoter

- Sale Transaction: Shares of FIITJEE Ltd. worth ₹90 crore

- Claim: Exemption under Section 54F for reinvestment in residential property

- AO’s Stand: Denied full exemption, citing multiple floors = multiple houses

- Court’s Verdict: All floors = one house = full exemption allowed

🏠 What Does Section 54F Say?

Under Section 54F of the Income Tax Act, if you sell a long-term capital asset (not a residential house) and reinvest the entire net consideration into one residential house in India, you can claim exemption from capital gains tax.

Key Conditions:

- You shouldn’t own more than one residential house on the date of transfer

- You must buy or construct a new house within 2/3 years

- Full exemption only if entire sale proceeds are reinvested

⚖️ What Did the Delhi High Court Decide?

- One House ≠ One Floor: The court held that multiple floors in a building used as a single residential unit should be treated as one house.

- Municipal Records ≠ Tax Interpretation: Just because SDMC records list different floors, doesn’t mean they are separate residential houses for income tax purposes.

- Disclosure Was Honest: The assessee had clearly disclosed the transaction and reinvestment. No intent to hide.

📜 Legal Takeaways

| Issue | Court’s Finding |

|---|---|

| Ownership of multiple floors | Still qualifies as “one residential house” |

| SDMC showing different units | Not sufficient to deny exemption |

| Honest disclosure by taxpayer | Strengthens the claim under Section 54F |

| AO’s reassessment | Overruled based on facts and legal clarity |

“The ruling is a clear application of the principle of substance over form,”

“This will help many genuine taxpayers whose properties are structured across floors but function as a single unit. The Delhi HC judgment sets a strong precedent.”

✅ What Should You Do?

If you’re planning to reinvest capital gains:

- Ensure actual usage of the house aligns with single residential use

- Keep documentation clear about unit configuration

- Don’t rely solely on municipal records—substance matters more

- Make full disclosure in your ITR

📌 Quick Recap Who Can Benefit from This Judgment?

- Taxpayers selling non-residential assets (e.g., shares)

- Planning to reinvest in one residential house

- Property structured across multiple floors but used as one unit

- Facing scrutiny based on property records

❓ FAQ on Section 54F and Multi-Floor Homes

Q1: Can I claim 54F if I buy a duplex?

Yes, as long as it’s used as a single house.

Q2: What if municipal records show separate units?

Courts look at actual use, not just how it’s recorded.

Q3: Will this help in ongoing reassessments?

Yes. This HC ruling can be cited as legal precedent.

📣 Need Help Claiming 54F Exemption?

Let Efiletax handle your capital gains filing.

Accurate. Timely. Legally Compliant.

👉 Talk to Our Experts Today